Today’s big news is that the June CPI inflation report came out with the headline CPI having a -0.1% decrease in prices from May to June, and the Core CPI for June had only a 0.1% monthly increase. These were both lower than the markets predicted, and these reports increased the market’s estimated probability of a Fed rate cut in September to now be 100%. This was the first decline in monthly CPI prices in four years.

The annual rate of CPI inflation was 3.0% in June, down from 3.3% in May, and the Core CPI, which strips out food and energy costs was 3.3% in June, down from 3.4% in May.

As a result of this increased probability of the first-rate cut happening in September, the MBS markets rallied this morning after these reports were released.

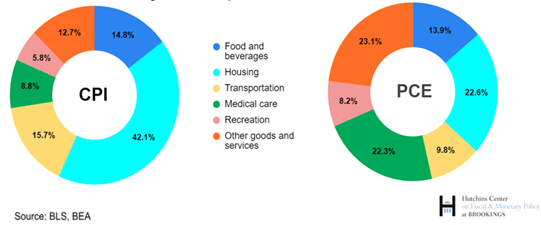

June CPI Report. The Consumer Price Index or CPI is one of two monthly inflation reports that attempt to measure the monthly change in price of a basket of goods that a typical consumer would spend their money on. The other monthly inflation report is the Personal Consumption Expenditures or PCE report. The reports measure similar expenditures such as food, gasoline, housing costs, entertainment costs, etc… but they have different weightings for the items in their basket. The graphs below show the different weightings.

How are inflation rates calculated? The calculation of inflation is very straightforward. It is literally how much did the price for the entire basket of goods and services change from one month to the next. That is the monthly rate of inflation, and the total of the monthly increases for the last 12 months is the annual rate of inflation. So, if the monthly increases are 0.3% each month for 12 months, then the annual increase would be 3.6%.

Many economists like to also look at the “Core” CPI or PCE inflation data, which takes food and energy prices out of the basket, not because they are not important consumer expenses, but because these prices can vary greatly from month to month due to weather, or other factors not related to the direction of the economy. By removing these two items and looking at the remaining “Core” items, we can see a better trend of inflation in the economy.

The reason all of the above is relevant to our mortgage industry is that the Federal Reserve’s official objective is to get the Core PCE inflation down to 2.00%, and they will need to feel confident that the PCE report is trending to this direction in order to consider doing rate cuts.

Impact to the Fed. Today’s surprisingly low Core CPI report is giving the markets hope that the June Core PCE report will come in lower than previously anticipated, and this will increase the Fed’s confidence to lower rates.

The next Fed meeting is at the end of this month, on July 30-31. The markets are not expecting the Fed to announce a cut at the end of this meeting, but they are hoping that the Fed’s official statements on July 31 will reflect increased optimism from their previous meetings that we would see rate cuts this year.

After today’s surprise CPI report came out, the Fed Futures market is pricing in a 100.40% probability of a Fed rate cut of 25 basis points in September, a 79.6% chance of a second Fed rate cut in November, and over a 100% probability of a third rate cut by next January.

If the above rate cut timeline actually occurs, the MBS market will rally in advance of these expected cuts, and mortgage borrowers will see lower rates before the official Fed decisions are made. In contrast most HELOC borrowers will not see their rates drop until after the Fed decisions are officially announced.

This Market Update and similar such communications are for informational purposes only and are based on publicly available information. These materials are general communications, which are not impartial, and are provided solely for discussion purposes, and not in connection with any product or service offering. The opinions and views expressed in this Market Update are as of the date of this communication and are subject to change. Any forward-looking views and statements contained in this Market Update are based on current estimates or expectations of future events or results. Actual results may differ materially from those described in this Market Update. The views expressed in this communication should not be attributed to Guild Mortgage Company as a whole and may not be reflected in the strategies and products offered by Guild Mortgage Company.