MBS prices are a little better this morning, continuing Friday’s small price rally as the markets expect the economy may be slower than previously predicted for this year. The yield on the 10-year Treasury bond is presently at 4.408% which is its lowest level since December.

The impact to different Federal government agencies, both in potential jobs and spending cuts, is greater than many market investors had anticipated, and this is causing the markets to revise their 2025 economic forecasts slightly downward. Also, reduced government spending helps reduce the Federal budget deficit, which also creates a downward pressure on long term interest rates, by reducing the supply of Treasury bonds that must be issued to finance the deficit.

Yesterday’s elections in Germany have highlighted the friction between Germany and much of western Europe with the U.S. and these frictions are very evident with the NATO alliance, as well as tariffs. These tensions are adding to the market volatility in world debt markets, including the U.S. Treasury and MBS bond markets. This friction is discussed in detail below.

The uncertainty behind the efforts of DOGE to have access to data to audit spending, and the various legal challenges that are being filed fast and furious, are adding to the market’s uncertainty regarding trying to estimate the total amount of reduced spending in 2025. This does have an impact on the bond markets, and this is an additional added volatility to daily bond prices.

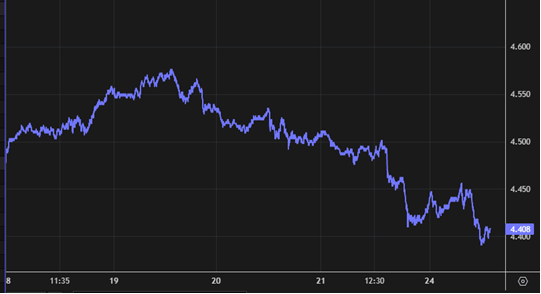

The markets are focused on the ongoing tariff negotiations and how these might impact consumer prices, thus impacting inflation and interest rates. The January PCE inflation report will be released this Friday. This is the Fed’s favorite inflation measure and their official target is to get the Core PCE inflation rate to 2.00%. The markets are predicting the January report will show a 2.6% annual rate and a 0.3% monthly rate of Core PCE inflation. The yield on the 10-year Treasury bond is currently down to 4.408% which is its lowest level of this year. This is about three basis points lower than Friday morning. Below is the graph of the 10-year Treasury bond yield over the last five trading days.

Home Prices. The National Association of Realtors (NAR) reported that home prices appreciated at an annual rate of 4.8% resulting in the median home price of $396,900. Tomorrow, we will see FHFA’s and CaseShiller’s home price estimates for December. The FHFA index is based upon the repeat sales data for the same property address for loans sold to Fannie Mae or Freddie Mac, and it showed an annual rate of 4.2% in November.

CaseShiller’s home price index is based on 20 selected metropolitan markets and is expected to show a 4.4% annual rate of appreciation.

Fannie Mae updated their home price appreciation forecast to be a 3.5% home price appreciation for 2025 and a 1.7% appreciation for 2026. These numbers have been dialed back a bit to reflect the increased uncertainties in the housing market.

The existing estimated 4 million gap in the supply of homes relative to the number of households and the fact that we are only building about 1.3 million new units per year does create an upwards pressure on home prices that may be in play for several years. The recent California fires, further added to this housing gap. With construction labor and materials expected to rise in 2025 due to these fires, and possibly due to tariffs, anything that adds to the cost to build a new home makes existing home values go up.

MBS Market Volatility. The markets will remain much more volatile than normal due to the rapid pace of political changes, and the continuing negotiations on trading relationships and tariffs, and how all of this might impact inflation rates or the size of the Federal budget deficit. For these reasons, it is very difficult for the markets to predict the future levels of interest rates. During these unusually volatile market conditions, usually the best strategy is to lock your rate rather than float – you simply have much more to lose if rates go higher and stay there for a long time, compared to if rates go lower and you can simply refinance to the new lowest rate.

This Market Update and similar such communications are for informational purposes only and are based on publicly available information. These materials are general communications, which are not impartial, and are provided solely for discussion purposes, and not in connection with any product or service offering. The opinions and views expressed in this Market Update are as of the date of this communication and are subject to change. Any forward-looking views and statements contained in this Market Update are based on current estimates or expectations of future events or results. Actual results may differ materially from those described in this Market Update. The views expressed in this communication should not be attributed to Guild Mortgage Company as a whole and may not be reflected in the strategies and products offered by Guild Mortgage Company.