MBS prices are about flat to yesterday morning. The only material economic report today was the University of Michigan Consumer Sentiment Survey which came out with a surprise 57.9 index for March, below the 63.1 market prediction and below last month’s 64.7. Normally reduced consumer confidence translates to reduced future consumer spending which reduces inflation pressures.

However, despite lower than expected CPI and PPI inflation reports this week, and today’s increased negative consumer sentiment, which normally reduce the market’s fears of inflation, the markets are more focused on how tariffs could impact consumer prices in the coming months and will trade issues between the U.S. and Canada, Mexico and Europe be resolved quickly or will tariffs be in place for a long time?

The biggest market news this week is yesterday’s confirmation of Bill Pulte to be the new Director of FHFA, which is the regulator of Fannie Mae and Freddie Mac. Pulte will be able to have a significant impact on the challenges facing the housing industry, as he has the authority to direct the strategies and activities of Fannie Mae and Freddie Mac.

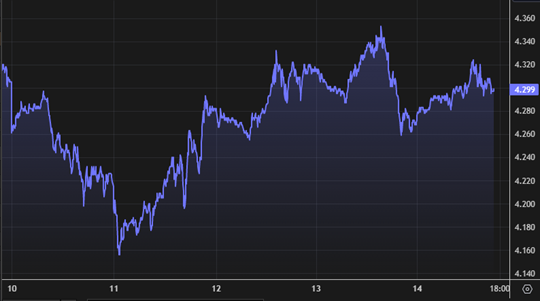

The Federal Reserve will have their next regularly scheduled FOMC meeting next week and the markets are predicting they will not make any rate cut. The markets are predicting the next Fed rate cut will happen at their June meeting, with a second cut at their September meeting and a third rate cut at their March 2026 meeting. These predictions will change as the markets’ perceptions about future inflation levels change. The Fed will slow down or stop cutting if they think inflation rates are increasing long term. The yield on the 10-year Treasury bond is currently at 4.299% which is effectively flat to where it was yesterday morning. Below is the graph of the 10-year Treasury bond yield over the last five trading days.

Market Details

Consumer Sentiment. The University of Michigan Consumer Sentiment Survey for March came out with a total index value of 57.9 which is well below where it was last month at 64.7 and below the market’s prediction of 63.1 for today’s report. The portions of the survey that reflect a person’s current condition came out at 63.5 for March, down from 65.7 in February. However, the portions of the survey based upon a person’s future expectations dramatically dropped to 54.2 in March from the 64.0 in February.

Most of this drop in consumer sentiment is attributed to the discussions of tariffs in the media, and in my opinion, most of the news stories have not been balanced. There are pros and cons on the use of tariffs to achieve fair and balanced trade relationships between countries. The overwhelming majority of media news stories about tariffs provide great detail on the possible negative impacts to U.S. consumers and businesses, with very little, or zero mention of any possible benefits.

Most media stories provide little or zero insight into how and why long-term trade deficits create long-term economic harm to U.S. consumers and businesses. Also, most media stories do not mention that other countries have had tariffs on U.S. goods for many years and that the U.S. is seeking to have the same reciprocal level of tariffs in order to achieve a more balanced trade relationship.

Tariffs and Trade Wars. Bipartisan economic research groups predict that a sustained trade war between the U.S. and Canada and Mexico would result in significantly more harm to Canada and Mexico than the U.S. and it would push Canada and Mexico into painful recessions. If this is true, it would create powerful incentives for Mexican and Canadian leaders to negotiate fair trade relationships, and they would have strong motivation to do this quickly to reduce the financial damage to their economies.

In my opinion, there is a very good possibility that the tariff wars between the U.S. and Canada and Mexico could be resolved by June. If this were to happen, it would reduce inflation fears in the markets, and this would be positive for long term interest rates such at the 10-year Treasury bond and mortgage interest rates.

Daily MBS Volatility. We will likely continue to see higher than normal daily price volatility in the MBS markets until bond investors become more confident in the long-term direction of inflation rates. Because most every mortgage rate sheet in the country is based upon daily price changes in the MBS markets, the increased daily price volatility in MBS markets will translate 1:1 to increased daily volatility in mortgage lender rate sheets for the next several months.

Every borrower who chooses to float in a volatile market is making a 50/50 bet every day they float that they will get a better or worse rate sheet on the next business day. There is no human being on the planet who can predict which direction tomorrow’s MBS prices go better than a 50/50 probability. If you don’t believe this, it is very simple to prove. We can just take each day’s “float” or “lock” prediction and compare it to the next day’s good or bad rate sheet price change. After about ten compares we will see that each day’s prediction is only accurate 50% of the time.

If a person is advising to float today, this implies that tomorrow’s rate sheet will not be worse. This is only correct 50% of the time, and this is bad advice 50% of the time.

When MBS markets are not volatile, and there are small or zero daily rate sheet changes, a floating borrower is risking gaining or losing a relatively smaller economic gain or loss with their 50/50 daily betting odds. However, in volatile MBS markets like we have today and will likely have for several months to come, the borrower who enjoys taking 50/50 daily betting odds is risking losing much higher economic harm than the benefit they may gain.

A purchase borrower could risk no longer being able to qualify if rates go high enough or being stuck with a much higher interest rate for potentially a very long time. A floating borrower is risking much less, because if rates drop, they can refinance to the new lower rate, so their only economic loss is having the higher rate for the relatively short time period until they refinance, where a floating borrower could face a higher rate for a much longer time, period and possibly forever.

Locking a rate during the application process for a purchase mortgage loan provides incredibly powerful financial protection to a home buyer. To forgo this protection in the 50/50 hopes of getting a better rate sheet price may not be a great risk/reward tradeoff for a purchase borrower.

This Market Update and similar such communications are for informational purposes only and are based on publicly available information. These materials are general communications, which are not impartial, and are provided solely for discussion purposes, and not in connection with any product or service offering. The opinions and views expressed in this Market Update are as of the date of this communication and are subject to change. Any forward-looking views and statements contained in this Market Update are based on current estimates or expectations of future events or results. Actual results may differ materially from those described in this Market Update. The views expressed in this communication should not be attributed to Guild Mortgage Company as a whole and may not be reflected in the strategies and products offered by Guild Mortgage Company.