The May Consumer Confidence report came out this morning much stronger than the markets had predicted, at 102.0 compared to the market’s prediction of 95.9. The U.S. stock markets have been trading at record highs in the last six months in anticipation of Fed rate cuts starting this year. When the Consumer Confidence report came out this morning, stock prices did not move, and the bond markets traded off slightly. But then Minneapolis Fed President Neal Kashkari made public remarks that he thinks the Fed should wait longer to lower rates, and that he thinks a rate increase is very much on the table, undercutting Fed Chair Jerome Powell who previously said he does not see the Fed doing any more rate increases.

The combined result of the stronger than expected Consumer Confidence report, plus Kashkari’s wet blanket comments about wanting to keep rates higher for longer than the markets are predicting, and his adding in the possibility of doing more rate increases, has driven bond prices slightly lower than their closing levels last Friday. However, the bond markets did rally a little just before closing on Friday, so today’s rate sheets are currently about 12 basis points better in price than on Friday morning, despite the not-so-great news for bonds this morning.

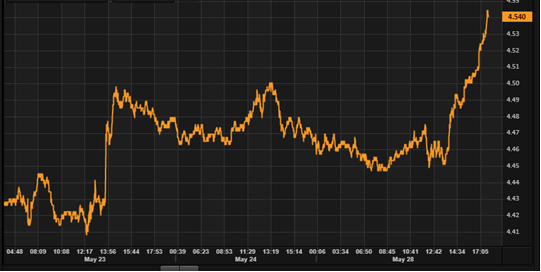

The Fed Futures markets are presently predicting about a 51% chance that the Fed does a rate cut in September. The yield on the 10-year is presently 4.540% which is almost seven basis points higher than its level on Friday morning just before the three-day holiday weekend’s early market closure.

Market Details

Consumer Confidence Report. The markets had predicted that the May index would come out at 95.9 which would have been a decline from April’s 97.0 index. This morning’s report coming out at 102.0 shows the market was wrong both in their estimated direction of this index and in the level of the index. Given that consumer spending drives about 2/3rds of all U.S. economic activity, this is normally considered to be a good insight into future consumer spending levels, which would then translate to higher economic activity, and thus create upside inflationary pressures. The Fed is hoping that their rate increases are decreasing consumer confidence, which would then slow down inflationary pressures.

However, as our economy recovers from the high levels of government stimulus during the COVID recession, there have been times when changes in consumer sentiment did not always correlate to changes in future actual spending levels. Even though consumers were in a grumpy mood, many still had larger levels of cash savings due to the stimulus programs, so they continued to spend at above normal levels. For this reason, the markets are placing more emphasis on actual consumer income data and actual spending levels, rather than on future looking sentiment indices.

If there is any surprise in today’s report, it is that the bond markets did not trade off further this morning due to the much stronger consumer sentiment report at the exact same time the Fed was hoping to see a slowing consumer sentiment and thus a slowing economy.

Wednesday’s Reports. There are no material reports scheduled. Fed speakers would likely be the source of any volatility in MBS prices tomorrow.

Thursday’s GDP Report. The bond markets are looking past today’s Consumer Confidence reports to see Thursday’s second estimate of the GDP for the economy in the first quarter of this year, which is predicted to show a 1.3% rate of GDP which would be lower than the initial estimate of 1.6%, and lower than the final GDP of 3.40% for the fourth quarter of last year. Because there is a large amount of data and calculations in the GDP number, which measures the entire output of the U.S. economy, the Department of Commerce releases an initial estimate, then a second estimate, and then a final estimate.

If Thursday’s GDP report comes out lower than 1.6%, it will tell the markets that the economy was slowing down in the first quarter of this year, and if this slow down continues in the second quarter, this will put the Fed in a good position in September to consider a rate cut. If this report comes out lower than 1.3% tomorrow, this will tell the markets that the economy is slowing down more quickly than previously thought, which will increase the probability of the Fed doing a rate cut in September, with July becoming a slim possibility, and this would cause a rally in the bond markets on Friday. If the number comes out higher than 1.3%, this would tell the markets that the economy was not slowing as fast as predicted, and this would create a downward pressure on MBS prices.

Friday’s PCE Data. These will likely be the most impactful reports this week on MBS prices. The Personal Consumption Expenditures reports are the Fed’s favorite measure of inflation, and it is the Fed’s stated goal to have the Core PCE inflation report hit a 2.00% target. The Fed will not cut rates until they view this inflation report is on a clear path to this target.

The markets are predicting that the Core PCE inflation report for April will show a 0.3% monthly increase and an annual rate of 2.8% Core PCE inflation. This would be flat to March’s levels.

As a reminder, the Core PCE report measures the monthly price changes in a basket of goods that the average consumer would spend their money on each month. The “Core” report strips out food and energy prices from this basket because their prices can be volatile from month to month based upon weather patterns or other short-term factors, and this volatility can mask the overall longer-term trends in the broader economy. Also, important on Friday will be the Personal Income report which is expected to show a 0.3% monthly increase in April, down from March’s 0.5% increase. If incomes are higher than predicted, this would likely lead to increased future consumer spending, which would then push up inflation levels, and thus push back further the timing of the Fed’s first rate cut.

This Market Update and similar such communications are for informational purposes only and are based on publicly available information. These materials are general communications, which are not impartial, and are provided solely for discussion purposes, and not in connection with any product or service offering. The opinions and views expressed in this Market Update are as of the date of this communication and are subject to change. Any forward-looking views and statements contained in this Market Update are based on current estimates or expectations of future events or results. Actual results may differ materially from those described in this Market Update. The views expressed in this communication should not be attributed to Guild Mortgage Company as a whole and may not be reflected in the strategies and products offered by Guild Mortgage Company.